Key Takeaways

- The Middle East conflict has clouded the UK's improving inflation outlook, with prices expected to remain above target through 2026.

- Surging fuel and fertiliser costs are squeezing UK farmers and food retailers, threatening to push consumer prices higher.

- Shaken consumer confidence is curbing spending, limiting how much retailers can pass on rising costs.

The economic consequences of the conflict in the Middle East evoke parallels to those seen in 2022, resulting from the Russia-Ukraine conflict, as energy and production costs soar. With the current UK economic climate highly sensitive due to sticky high prices, strained public finances and low confidence and the UK government keen to kickstart growth, it’s no surprise that many households and businesses are concerned. Food prices are particularly vulnerable to this shock while also being a top priority for consumers, putting them back in the spotlight once again. With producers and consumers already under strain, how is the conflict expected to shape the food sector?

The onset of 2022 brought significant economic headwinds encapsulated by a now well-known phrase – “cost-of-living crisis”. Russia’s invasion of Ukraine in February 2022 caused global energy prices to climb as supplies of oil, gas and coal were squeezed and sanctions on Russian exports were implemented. In turn, energy prices in the UK soared, with the Office for National Statistics (ONS) reporting that the average electricity price for UK non-domestic users shot up from 14.81 pence per kilowatt hour in the first quarter of 2021 to a high of 28.39 pence per kilowatt hour in the fourth quarter of 2023 – this is a hike of more than 90%. With inflationary pressure already building in late 2021, these higher energy prices trickled through into skyrocketing inflation as the price of fuel rose alongside domestic energy prices, which also fed through into the cost of producing other goods and services for businesses. Other factors, such as poor weather that reduced harvests and rising fertiliser costs due to the conflict, put further pressure on costs.

ONS data shows that consumer price inflation reached a staggering 11.1% in October 2022. With prices soaring, consumer confidence tumbled, restricting spending and creating a demand shock for many businesses. Subdued customer spending, alongside wage and tax hikes, caused business confidence to drop, too. As a result, GDP growth has stagnated, creating a negative atmosphere around the UK’s economic performance.

Initially, 2026 brought some much-needed optimism. The Bank of England’s February 2026 Monetary Policy Report provided the long-awaited good news that although consumer price inflation was currently above 2%, it expected it to fall back to this target from April in response to changes in energy prices following the 2025 Budget. This boded well for consumer confidence and spending, which would feed through to stronger business performance over time.

The ongoing conflict in the Middle East, resulting from clashes between the US and Iran that began in February 2026, has reintroduced uncertainty surrounding energy supply and prices, threatening to dent confidence and spending once again. The Bank of England’s April 2026 Monetary Policy Report underscored this sentiment, noting that the conflict has made the outlook for global energy prices highly uncertain and that inflation is expected to be above the March 2026 rate of 3.3% by the end of the year. Additionally, in April, the International Monetary Fund (IMF) slashed its estimate for UK GDP growth for the year from 1.3% to 0.8%, the biggest downgrade for the largest of the world’s advanced economies. The organisation cited the conflict, fewer interest rate cuts and lingering high energy prices as reasons for this. This evokes parallels with the 2022 energy crisis, which won’t be a welcome feeling for Brits. The shock is expected to deal a blow to UK businesses as they continue to seek the light at the end of the tunnel, as well as the UK government, which has placed a large emphasis on driving economic growth.

The Causes of Concern

The conflict in the Middle East is causing major disruption to the normal supply of goods, including oil, gas and fertiliser, as shipping routes and energy facilities face disorder. One of the largest drivers of these negative supply shocks has been the closure of the Strait of Hormuz. The International Energy Agency reports that around 25% of the world’s seaborne oil trade passes through the strait, alongside 20% of global liquefied gas exports. Around one-third of the global seaborne fertiliser trade also passes through the strait, reports UN Trade and Development.

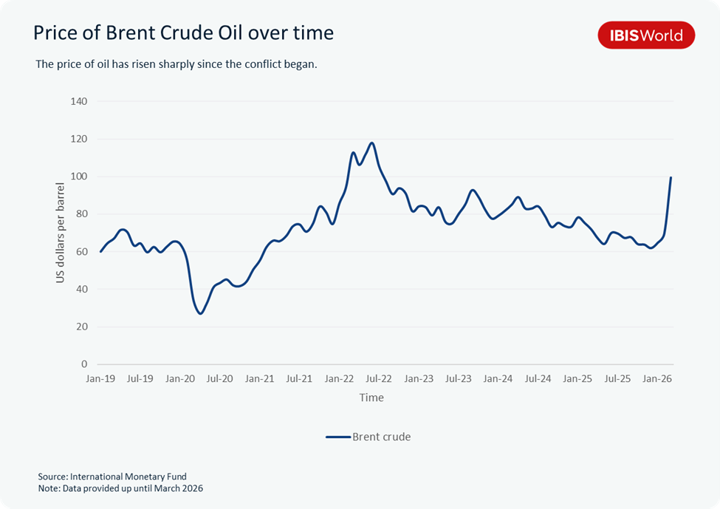

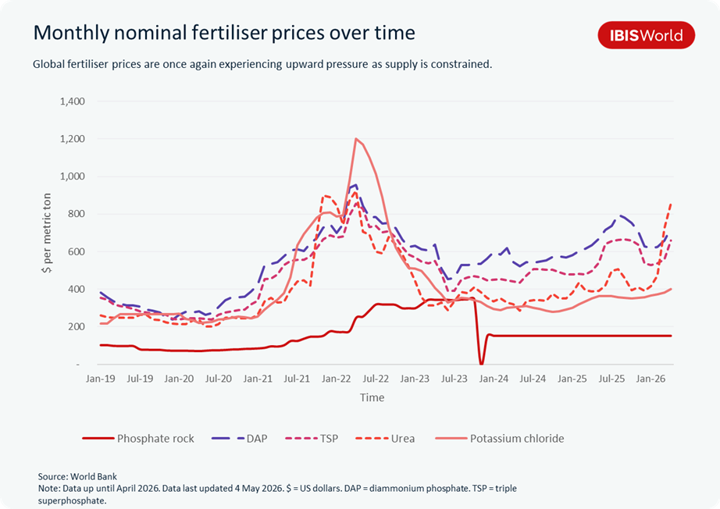

Extensive supply constraints are pushing up the prices of key inputs to goods and services. Data from the IMF reveals that Brent crude oil prices climbed by 43.2% in March 2026. Red diesel, a critical input for the agricultural industry in the UK, has also made significant gains, rising by 19.6% in March 2026, followed by a 31.2% hike in April 2026, as shown in data from the Agriculture and Horticulture Development Board (AHDB). Additionally, the price of fertiliser has soared, primarily due to movements in gas prices, with the cost of Granular Urea 40.9% higher in April 2026 than in February 2026, as per the AHDB. At the same time, the cost of shipping goods has risen due to uncertainty about shipping safety in the area, leading to higher insurance premiums and re-routing, as well as higher fuel prices. In a May 2026 interview with Bloomberg TV, Maersk CEO Vincent Clerc stated that uncertainty over the Strait of Hormuz is costing the shipping and logistics company US$500 million (£368.1 million) per month, with those costs being passed on to consumers.

The Financial Cost of Conflict to the Food Industry

The whirlpool of spiralling costs is expected to have major implications for UK businesses, particularly those in the food sector. Food manufacturers and growers rely heavily on goods that are enduring upward pressure from the conflict – fuel and fertiliser. These inputs are necessary for transporting and producing goods. The crux, however, is that profit has already been spread thin due to the high inflation seen in 2022-23. Already struggling with weak returns, manufacturers and growers are expected to pass on at least some of these costs to retailers. These price hikes could fuel inflation once more, in a similar way to the cost-of-living crisis.

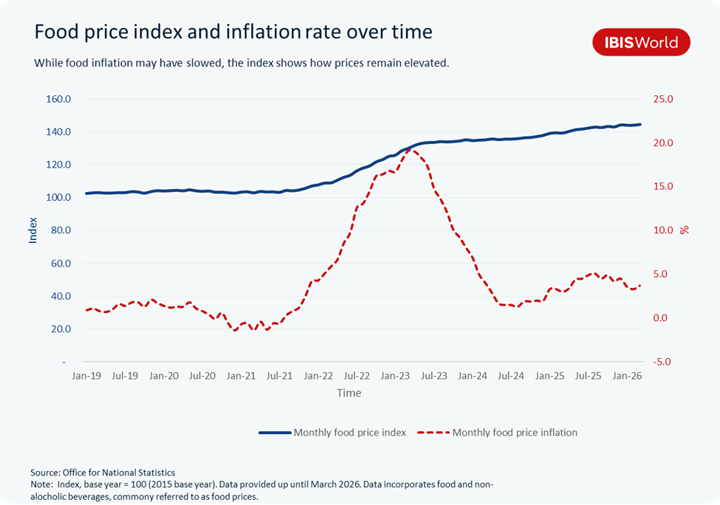

The impact will likely be seen over time as the rising costs slowly trickle through the supply chain. For example, ONS data show that food price inflation peaked at 19.1% in March 2023, over a year after Russia’s invasion of Ukraine. While this implies no immediate jeopardy, it could once again lead to a drawn-out period of uncertainty, low confidence and reduced spending, weakening economic growth.

The uncertainty surrounding the conflict's longevity adds a new layer, with implications that worsen the longer the conflict continues, as producers' and suppliers' ability to absorb additional costs weakens over time because taking a hit to profit becomes less feasible in the long term. In an April 2026 interview with the BBC, the chief secretary to the prime minister, Darren Jones, illustrated this concern by stating how higher prices could be expected for eight months or more after the end of the conflict.

Industries Affected

Farming in the UK:

One UK industry likely to be among the worst hit by the economic consequences of a prolonged conflict is food production. While existing stocks will provide a cushion for a period of time, they aren’t infinite. Numerous inputs are becoming more expensive, including energy, fertilisers and transport. Data from the AHDB shows that the price of Granular Urea, a key fertiliser, was 39.2% higher in the week of the first of May 2026 compared to before the conflict. As key inputs, these higher prices will feed through to higher production costs and profit will take a hit. The latest estimates from the Andersons Centre, a UK farming consultancy, reveal that agricultural input inflation rose to 8.4% in the 12 months to April 2026.

The rate of agricultural input inflation is currently below the highs seen in 2022. However, producers face an added layer of complexity: unlike in 2022, output prices haven’t moved in the same direction. For example, wheat, sunflower oil, maize and barley all experienced numerous price hikes as the Russia-Ukraine conflict disrupted global supply. Data from the International Grains Council (IGC) shows that wheat prices peaked in May 2022, when they were 66.9% higher than a year earlier. However, IGC data shows that grain prices are widely holding steady in 2026 compared to 2025. Dairy production has also been particularly hard hit. Data from Defra shows that in December 2022, farm-gate milk prices in the UK were 49% higher than in December 2021, as input cost hikes were passed on and demand remained high. However, the dairy industry is currently experiencing a supply glut that’s pushing prices down. The AHDB reports that in February 2026, average UK farmgate milk prices were down 21.7% compared to a year ago. With costs rising while prices are falling, the dent to profit is expected to be significant.

In response, food producers could look to renegotiate contracts with buyers, like supermarkets and other grocery retailers. The president of the National Farmers’ Union told the BBC in March 2026 that while some cost hikes can be absorbed, others will inevitably be passed on to consumers. Failing this, some producers may look to reduce fertiliser usage and reduce planting sizes to keep operations viable. However, this could significantly reduce supply by shrinking farmed areas and yields of certain crops, driving up prices over the longer term.

Supermarkets in the UK:

With producers facing higher costs and seeking to negotiate higher selling prices, consumer prices could swell as food retailers seek to offset the impact on profit. Compounding this is the fact that supermarkets don’t just buy from domestic producers. Defra data reveals that in 2024, 43% of food consumed in the UK came from outside the country. This makes the food supply chain particularly vulnerable to this global shock, as growers in other climates face a more immediate impact from fertiliser hikes as they enter their growing season, while transport costs have soared. Underscoring this concern, on 4 May 2026, the Energy and Climate Intelligence Unit revealed that UK food prices are on track to be 50% higher by November 2026 than at the start of the cost-of-living crisis in mid-2021.

Despite food retailers facing pressure to pass on cost increases, their ability to do so is likely to be much weaker than in 2022, as the cost hikes consumers will tolerate are lower given the previous dramatic increases. Research from the UK Parliament highlights that between November 2020 and November 2025, UK food prices swelled by 38.6%. The British Retail Consortium reported in May 2026 that 80% of people in the UK are concerned that the Middle East Conflict will raise food prices. As a result, consumer demand is highly sensitive, as even though food is a necessity, households may alter their shopping habits in light of rising prices. This could include trading down to cheaper alternatives, reducing basket sizes and shifting their spending to discount providers.

Concerns about the potential impact on profit from changing purchasing behaviours could create hesitation about immediate price rises, potentially keeping a lid on inflation. The British Retail Consortium (BRC) has already noted that retailers are absorbing a large number of additional costs arising from the conflict. However, because of this, supermarkets are likely to be tough negotiating partners for food producers, making it harder for producers to protect their own profit. This scenario is unlikely to hold over the long term, though, as it won’t be viable for supermarkets to continue absorbing rising costs as the conflict continues. The BRC also notes that pressures from the conflict will filter through via higher retail prices over the coming months.

Restaurants and Takeaways in the UK:

The expectation of further food price rises adds unwelcome strain to the UK hospitality sector, particularly restaurants and takeaways. The industry is already struggling against high labour costs and business rates, as well as elevated prices in food categories like beef and coffee. However, the main current concern for the food retailing sector is energy price rises rather than food prices themselves, as the conflict in the Middle East hasn’t directly led to increased ingredient prices through supply shortages, unlike the Russia-Ukraine conflict. This was noted by Greggs' CEO, Roisin Currie, in a May 2026 interview with Retail Week, where she stated that the business hasn’t seen ingredient shortages and none are predicted. As a result, the impact of rising food prices will take longer to trickle through to this sector, as it sits at the end of the supply chain. Greggs’ trading update for the first 19 weeks of 2026 underscores this by stating that it’s “monitoring the situation in the Middle East and should the conflict continue and become prolonged we, like all food retailers, will likely see higher overall cost inflation through the end of 2026 and into 2027.”

Although mounting food costs related to the conflict may not be an immediate concern for the food retailing sector, negative demand-side effects are. Eating out is a luxury for consumers compared to shopping for food in supermarkets, making demand more price-sensitive. PwC’s Consumer Sentiment Survey for Spring 2026 reveals that consumer confidence experienced the sharpest quarterly decline since the onset of the Russia-Ukraine conflict, with consumers intending to cut back spending in response. It also highlighted that spending in the “eating out” category had the largest negative net spending intention (the difference between the proportion of consumers intending to spend less versus the proportion intending to spend more over the next 12 months), at -32% in April 2026, with “going out” a close second with -30%. In comparison, “grocery shopping” had the largest positive spending intention at 27%, although this was down from 32% in January 2026. This highlights how the food service sector is more vulnerable to changes in consumer spending, raising concerns at a time when profitability is under strain.

Final Word

The economic consequences of the conflict in the Middle East for the UK are likely to be significant, particularly for the UK food sector, given its vulnerable position as an energy and food importer. However, the true impact is likely to materialise later in the year.

While the severity of the impact will largely depend on the longevity of the conflict, it’s clear that some damage has already been done. If prices of key inputs like energy and fertilisers remain elevated by the time UK food producers need to renegotiate price contracts, the impact on the consumer will be felt through higher retail prices.

While parallels can be made between these events and those seen in 2022, there are clear distinctions. Firstly, UK agricultural output prices aren’t currently being pushed up directly by the conflict, unlike previously seen with ingredients like wheat, which fuelled inflation significantly and put the food retailing sector under immediate strain while providing a profit cushion for farmers. However, this could change the longer the conflict continues.

Additionally, consumers’ tolerance for higher prices is considerably weaker, as spending power has already been eroded. Retailers are likely to restrict the amount passed onto the consumer through higher prices in the near term so as not to significantly dent demand. Although this is good news for the consumer, it does mean that the UK food sector’s profit is likely to weaken. Moreover, this doesn’t bode well for economic growth, with both consumers and businesses retreating back into insecurity and left to question when things will truly get better.